Catastrophic Medical Claims: Risky Business

The COVID-19 pandemic is one of the most significant global threats to financial stability we have seen in our lifetime. The economic decline was steep and swift through April and it will likely be a long, slow trajectory back up to prior levels. The global output lost during the first half of 2020 is not expected to be recovered until late into 2021; for some countries, recovery may take even longer. Additionally, we anticipate that the structural job loss will take years to restore.

The economics of the pandemic have forced many companies to focus on preserving cash and defend their financials. With earnings under intense scrutiny, risk management decisions made previously may not be applicable or appropriate today. If you are currently sponsoring a self-insured group health plan, now is the time to take another look at mitigating this risk.

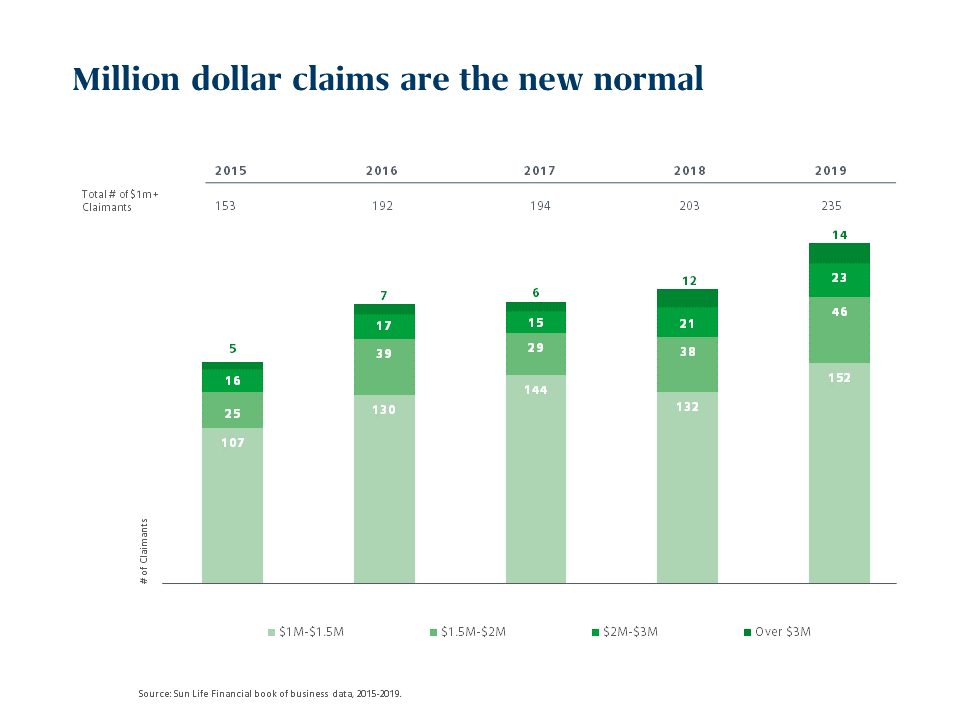

The single biggest threat to employer health budgets is catastrophic medical claims. Over the last several years, due to medical advances, the pattern and the nature of these claims have changed significantly. Both the frequency and size of catastrophic medical claims are trending ever upwards. We’ve now seen claims of $20 million or more – numbers that were once unimaginable. In addition, the nature of some large claims is changing as well. For some kinds of conditions that require ongoing treatment, very large claims are not one-time shock events that recede the following year. Instead, claims spike and then stay at that level, like an annual annuity.

Catastrophic claims can have a major impact on budgets and overall company financials, even moving the needle on earnings per share (EPS). For example, let’s say Company A is a large employer with 10,000 employees in their self-insured group health plan and doesn’t purchase stop-loss insurance today. What would happen to EPS if they were hit with a single $10 million catastrophic claim. Assuming all other operational budgets performed as expected, Company A’s EPS would drop from $3.08 to $3.02. That's a pretty big negative earnings surprise for any employer. If Company A had purchased stop-loss insurance, the coverage could have smoothed out the impact of that $10 million claim and EPS would have only dropped from $3.08 to $3.07.

Options for employers include transferring the risk through direct stop-loss markets or through a collective purchasing arrangement like Mercer’s Stop-Loss Coalition where insurers agree to enhance coverage with exclusive multi-year rate caps, no new laser provisions and profit sharing. Large employers looking to buy stop-loss with deductibles in excess of $1 million may find it difficult to buy coverage through the traditional stop loss market. In that case, a captive insurance company may be the most viable option. Some companies choose to use their own single parent captive to access reinsurance markets or to pool the risk with other organizational risk (e.g. property and casualty). Others pool their medical claims risk with other like-minded organizations through a group captive arrangement.

The pandemic has taught us that sticking your head in the sand and hoping for the best is not a solid business strategy. Companies that didn’t have adequate business continuity coverage heading into the pandemic learned that lesson the hard way. You may reassess your situation in light of the current economic environment and still deliberately choose to assume all the risk of catastrophic medical claim risk and the associated financial impact. But if you choose to transfer that risk, it’s important to consider all of your options, including the potential use of a captive. No matter what decision you’ve made in the past, the changing nature of catastrophic medical claims and the current economic crisis make a stop-loss evaluation a business imperative for employers of all sizes.

For more information about stop-loss insurance or medical captives contact Dan Davey, Rich Fuerstenberg or your Mercer consultant.